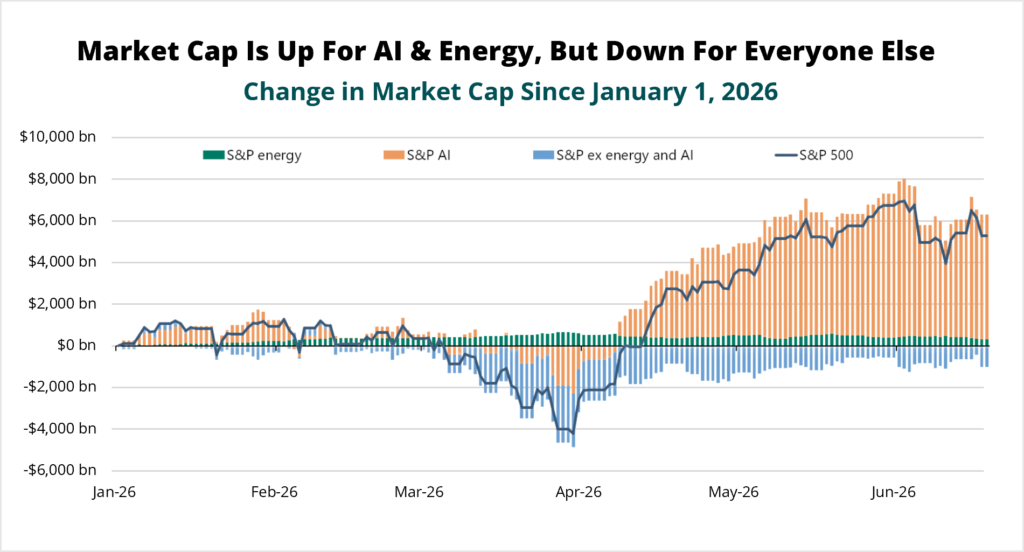

Equities surged in the second quarter (Q2) as investors anticipated an end to the Iran war and shifted their focus back towards expectations for artificial intelligence and U.S. corporate earnings growth in 2026. Crude oil prices reverted to pre-crisis levels, consistent with the experience of the nine prior major oil-related regional wars since 1980, where prices averaged 4% lower six months after conflict began than they were before the war. Whether the tenuous ceasefire holds remains to be seen, but with OECD inventories having fallen to levels not seen since 1990, a renewed disruption could still precipitate an oil price and supply chain shock that current equity prices are not discounting. Meanwhile, the TSX appreciated 7%, while the S&P 500 rose 15%, its best quarter since the Q2 2020 COVID-19 rebound.

While commentators ascribe the market’s ascent to the S&P 500’s estimated 25% earnings growth in 2026, the current artificial intelligence (AI) narrative is inseparable from both. Since the March lows, the S&P 500’s rally has been overwhelmingly driven by AI-related stocks while the rest of the market has contributed relatively little to the index’s gain. Ten stocks alone drove 78% of the S&P 500’s Q2 return, eight of which were semiconductor related businesses benefiting from the AI data center buildout.

Source: Bloomberg, Apollo Chief Economist

Roughly half of the S&P 500’s expected earnings growth can be attributed to the buildout of AI infrastructure as ~$750 billion in hyperscaler capital expenditure directly translates into revenue and earnings growth for microchip and equipment suppliers. Semiconductor earnings alone are expected to rise 133% this year, while businesses such as Caterpillar, whose generators are being deployed to power AI data centers, are expected to grow earnings by nearly 30%. Factor in SpaceX’s record $1.8 trillion IPO in Q2 at a valuation of nearly 100x revenues, much of which depends on future data center growth expectations, as well as Anthropic’s and Open AI’s near trillion dollar anticipated public offerings in coming quarters and the market narrative is overwhelmingly one of AI and growth.

There are many reasons the current environment could persist for some time. Annual data center capex is expected to rise towards $1 trillion, perhaps by as early as 2027; frontier models continue to scale exponentially; and the adoption of AI in enterprise applications remains in its infancy. While the tailwinds for AI compute are undeniable, stock market narratives can and do change. When narratives about the future are deeply embedded into equity valuations and the plot unexpectedly changes, investors can find themselves uncomfortably exposed.

At the height of the Tech Bubble in 1999, Warren Buffett penned a prescient article in Fortune magazine explaining why investor return expectations were too high given starting valuations and how revolutionary technologies such as the automobile and the airplane transformed society and the economy but failed to create long-term value for shareholders because of competition. He elucidated: “the key to investing is not assessing how much an industry is going to affect society, or how much it will grow, but rather determining the competitive advantage of any given company and, above all, the durability of that advantage.”

There is much debate over whether the current moment for AI stocks is more analogous to the early days of the internet in 1995 or to late 1999. No one can know with certainty, but the distinction should be a moot point. The better questions are: what outcomes are equity prices discounting and how probable are they?

Regarding valuations, in our Q4 2025 Market Letter, we discussed how “picks and shovels” providers that sell equipment to data centers could have been bought cheaply in early 2025, with little to no premium paid for future data center growth. This is no longer the case. Caterpillar trades at ~38x estimated earnings versus its long-term average of ~16x, and the semiconductor index trades at ~16x revenue versus its ten-year average of ~6x. Investors have clearly priced many AI-related businesses to generate high growth and elevated profitability for years to come, despite structural uncertainties in a rapidly evolving environment. Whether the current valuations are justified may depend on some basic but difficult-to-answer questions such as:

- Who will become the eventual winners among frontier-model labs and how many winners will there be?

- To what degree will open-source models erode frontier models’ pricing power and, by extension, disrupt their ability to earn attractive returns on capital?

- Will hyperscalers eventually temper capex spending? Will enterprises throttle AI spending until tangible returns are clearer?

- Has the current supply bottleneck in semiconductors fundamentally restructured industry economics, particularly in memory, or is this a temporary demand/supply imbalance in what remains a cyclical industry?

In our view, the answers to these and other questions remain uncertain, but are crucial to understanding the durability of future outcomes for companies across the AI value chain. While growth is all but certain, the long-term shareholder value created by that growth is not a sure thing. If valuations were sufficiently low, investors might not need to answer all of these questions to ensure a margin of safety. Our experience with rapidly evolving industries, however, has been that it is difficult to find an adequate margin of safety when valuations are high.

Greener Pastures and Lower Hurdles

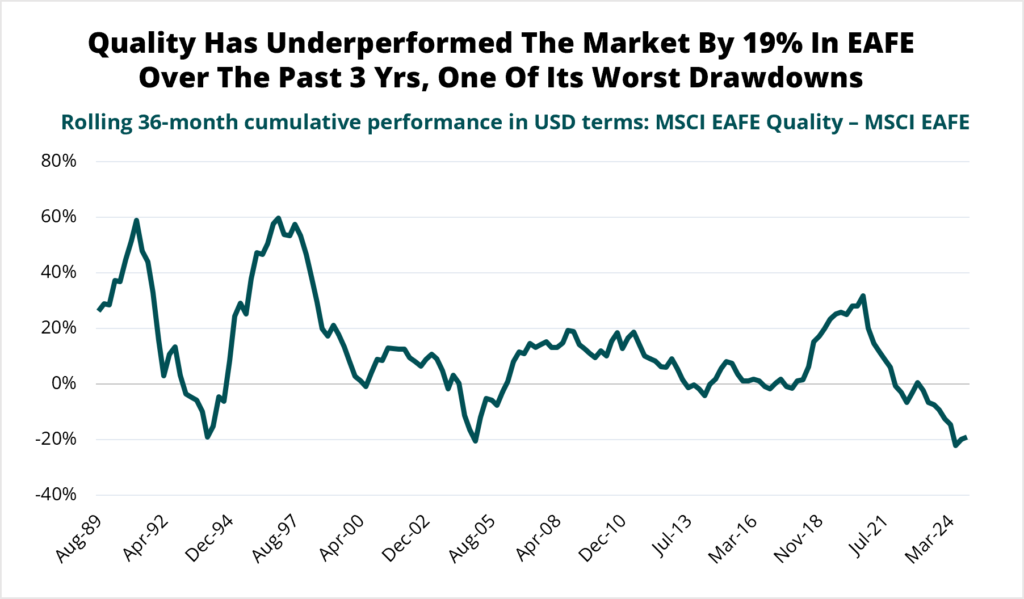

As investors have diverted capital toward the AI narrative, it has been funded from other areas of the stock market, driving valuations lower and consequently creating new opportunities. One of the most noticeable recent areas is among quality stocks with high, stable returns on capital, strong balance sheets and persistent earnings growth. This cohort typically trades at a premium to the market given its inherent characteristics, but recently many have fallen to rare discounts, likely because their near-term earnings growth rates are below those of the AI “winners” powering the S&P 500 higher this year. As shown below, European and Asian quality companies have underperformed the broader market to this degree on only two prior occasions. A similar situation has occurred in the U.S., spanning businesses across medical technology, pharmaceuticals, industrials, consumer discretionary and insurance.

Source: LSEG DataStream, MSCI, Schroders

Additionally, investors have taken a “shoot first, ask questions later” approach to perceived AI losers. Up until recently, the S&P 500 software sector was perceived as having among the most persistent pricing power of any industry because of its deep entrenchment within customer workflows. The sector traded as high as 40x forward earnings by 2021 as a result. In 2026 however, concerns that AI will disrupt software businesses have caused the sector to decline 17% to just 23x earnings, with many software and services stocks down 30% or more. Software’s decline not only illustrates how quickly a market narrative can change but also the resulting risk of underwriting extreme valuations against an uncertain future. Of course, many of the perceived risks driving down software stock prices have merit. Custom AI agents risk commoditizing rigid software platforms, while software and IT service revenue models – where value is derived through code built and integrated by armies of developers or through billable human hours – risk being disrupted by the compression of autonomous coding and engineering. However, for certain software companies, we expect the value of incumbency and deep integration into enterprise workflows to provide franchise durability, while others should be able to adapt their products and revenue model to an AI-driven future. The QV Canadian Equity Strategy has built its position in Constellation Software this year as valuations were pressured, while the QV Global Equity Strategy re-initiated Microsoft near the lowest valuation it has traded at in a decade. With both, AI-related concerns appear to be overblown.

As a software provider in mission-critical niches, Constellation should be somewhat insulated from AI disruption, while its strategy of value-accretive tuck-in acquisition should drive earnings growth for many years. We also think Microsoft’s leading position in AI infrastructure provides relevancy in a world where metered digital intelligence becomes an essential cost of doing business, ultimately strengthening its dominant software ecosystem.

Of course, our best ideas are often among businesses we already own. During the quarter, our equity teams added to multiple existing holdings where valuations had compressed, such as Intact Financial in the QV Canadian Equity Strategy, Stella-Jones and Stantec in the QV Canadian Small Cap Strategy and Netflix in the QV Global Equity Strategy. Broadly, valuations remain near long-term averages across our equity strategies, at a combined P/E of 15.7x. While certain areas of the market remain very expensive, we believe the opportunity set remains reasonable for value conscious investors.

Chasing Cars

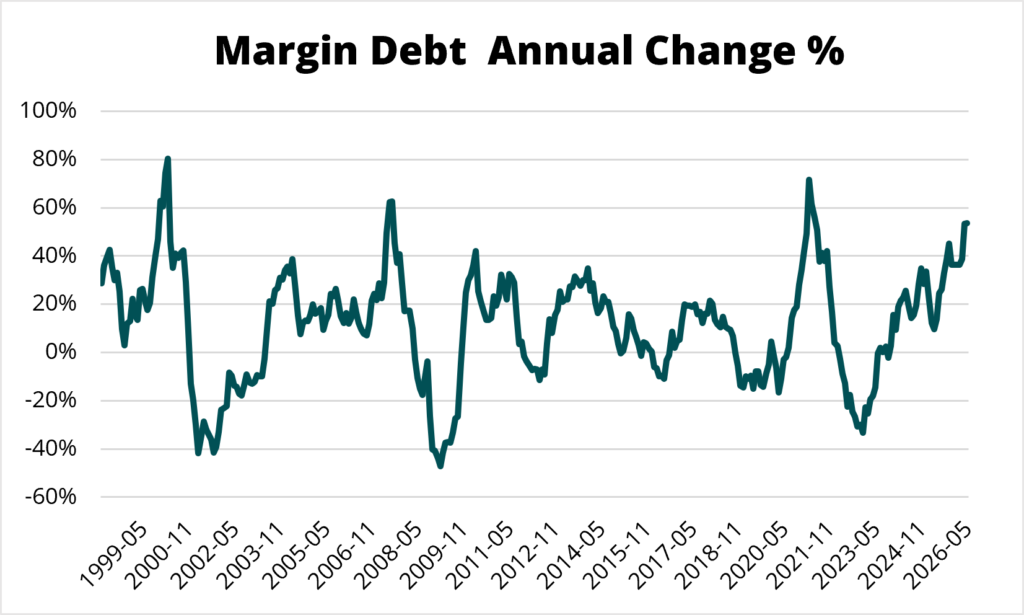

As a group, investors continue to lean into the excitement of the current narrative driving markets higher. Outstanding margin debt, which represents money investors borrow to buy stocks and is arguably one of the best indicators of animal spirits, has risen 54% in the last year – a level seen in only a handful of other periods late into bull markets.

Source: Finra

In an interview this May, Warren Buffett likened the stock market to a church with a casino attached, while suggesting that in more than 60 years of investing, “we’ve never had people in a more gambling mood than now. But that doesn’t mean that investing is terrible. It does mean that prices for an awful lot of things will look very silly.”

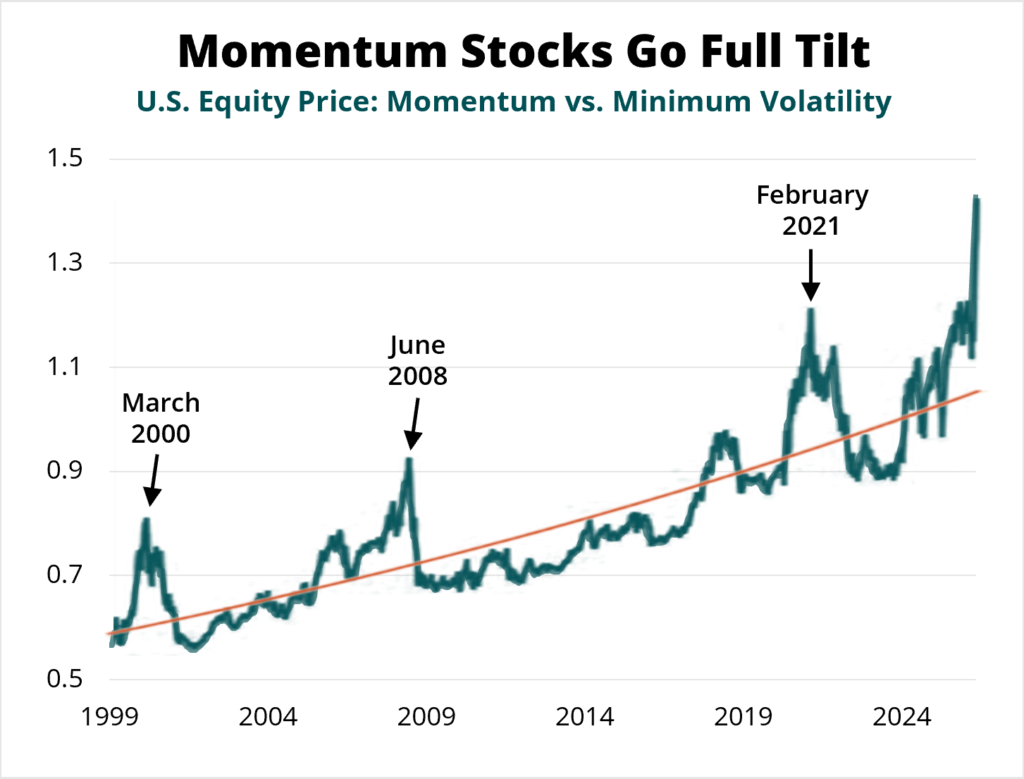

Apart from margin debt, momentum indicators are another way to monitor whether investors are in a gambling mood. ‘Momentum investing’ is a strategy of buying stocks whose earnings and stock prices have accelerated in the hope that it will continue without regard for valuation or long-term fundamental analysis. It is a trend-following behaviour that tends to gain traction in mature bull markets, either through outright commission or by omission as investors hold onto businesses far beyond what current earnings justify in the hope that the stock price will just keep on rising. That a number of institutional investors have recently pivoted their investing strategies to include momentum is perhaps a telling sign of the environment.

So far this year, ‘momentum’ stocks have risen to an extreme relative to much more mundane ‘low volatility’ stocks whose defensive businesses generate stable, predictable earnings. In the past, this has been a signal that exuberance in certain areas of the market may have gone too far too fast.

Source: MSCI, Alpine Macro

While strong earnings growth in 2026 could drive markets higher into year end, this does not mean investors should focus on current growth rates to justify a security’s valuation today rather than on the certainty and durability of its moat. Rather than chasing the excitement of the current narrative, we think the better risk-adjusted opportunities are in boring quality companies.