The Super Bowl Indicator emerged in the 1960s, stating that if an NFC team wins the Super Bowl, the stock market will rise, but if an AFC team wins, the market will decline. This indicator seems (rightly) nonsensical, which is why it’s surprising that it was remarkably accurate (90%+) for over 20 years. Statistically speaking, it would have been a 1-in-over-4-million chance that this indicator was accurate by coincidence alone. It turns out this indicator was indeed simply lucky because its accuracy fell off a cliff post 1990.

Predicting the future is hard – information that feels like a signal may well end up being noise (and vice versa). We start this overview of the QV Canadian Equity Strategy with this story to remind our clients and readers that QV is not a predictor of the future because we don’t think anyone can do it well consistently (even if they managed to get it right once or twice in the past). We invest based on a balance of probabilities, while diversifying our exposures to create the results we will discuss below.

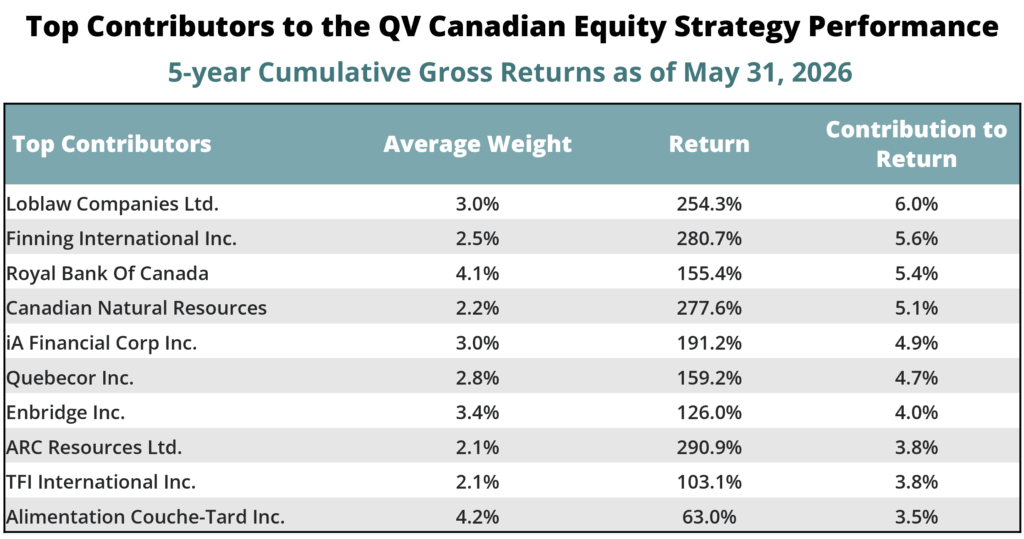

The QV Canadian Equity Strategy has posted strong absolute returns in recent periods – an average of 14% over each of the last 5 years, compared to our long-term historical average of close to 9% per year, ending May 31, 2026. Our benchmark, the S&P/TSX Composite TR Index, has seen incredibly strong performance over the same period, driven by commodity prices, bank outperformance and a low valuation base. We are happy with our performance, particularly given the risk we took to achieve it. Case in point, the largest contributor to our performance over the last five years was our investment in Loblaws – the largest Canadian food and drug retailer. While energy and financials investments like Royal Bank and Canadian Natural Resources were also top contributors to performance, our overall performance was driven much less by calling a commodity or economic cycle and more by buying good companies that were unloved and undervalued at the time.

Source: QV Investors

Despite a strong Canadian stock market, the Canadian economy is struggling to grow. In turn, we have been asked how we feel about the portfolio and our ability to protect against downside risk in this environment? Because we are not macro-economic forecasters, QV often gravitates towards companies that tend to do well in many economic environments (rather than companies that wildly thrive in one outcome and languish in several others). As such, we generally feel confident that our portfolio of investments will hold up well in a recession or trade war. By the same token, we acknowledge that, because we tend not to own companies that will disproportionately “win” when one set of circumstances happens, we tend to lag the index when an event (for example, a war in the Middle East) disproportionately benefits one specific sector while leaving all others unaffected (or hurt).

Within the strategy, strong performance has not come from the TSX’s largest winners (energy, gold or banks), but from companies that saw a normalization in valuation due to industry-specific factors.

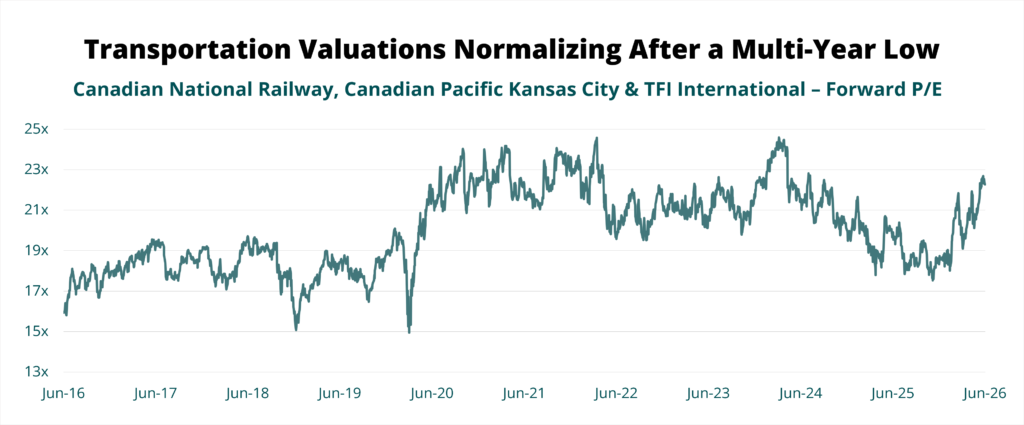

Our first example is the transportation industry. After a short-lived period of euphoria post COVID-19, these businesses went through a four-year recession in which the supply of transportation exceeded demand. Weak demand, rising input costs and trade war uncertainty saw high quality transport companies like Canadian National Railway, Canadian Pacific Kansas City and trucking company TFI International reach multi-year low valuations. We steadily added to our transportation holdings over the last two years as valuations fell. We are pleased to see initial signs of demand growth alongside signs of supply exiting the market, which has resulted in valuations normalizing in the sector.

Source: Capital IQ

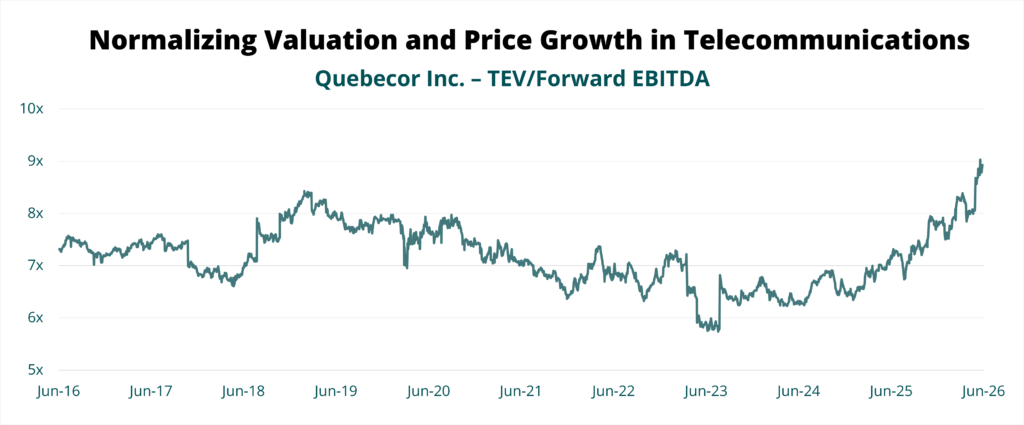

Another example was our foray into telecommunications. This industry had a difficult time dealing with rising interest rates due to high debt levels, a fierce price war in the wireless sector and overspending on infrastructure. We’ve seen decade-low valuations for all Canadian telecommunications companies. Given the state of each player’s balance sheet, our view is that rational behaviour (in the form of pricing) is an eventual necessity in order to achieve broad de-leveraging. In the same vein, given balance sheet constraints, we believed that capital spending discipline would also be necessary. Lastly, we felt that the valuation we needed to pay to become a shareholder was quite attractive. With this context, we felt Quebecor had the strongest balance sheet of its peers, the highest free cash generation, and a historically low valuation level. In contrast, the valuations for many other defensive sectors had been bid up to relatively unattractive levels. We have enjoyed good share price performance as Quebecor’s valuations have normalized over the last 12 months.

Source: Capital IQ

Looking forward, we continue to see interesting places to allocate capital. Recent fears over AI have materially dragged down valuations for otherwise high-quality companies across multiple sectors. For the first time in many years, QV is now a shareholder of Constellation Software (CSU) again, and we have slowly continued to add to our position. Fears of AI disrupting the company’s business model have more than halved its valuation in the market today, despite the company continuing to put up 20%+ earnings growth. Year to date, CSU is hitting record levels on the number of acquisitions it has made, which we think bodes favourably for future growth. In the same vein, fears that AI will replace human consultants have also resulted in very low valuations for CGI and WSP Global. We believe these fears are overblown, given that CGI and WSP hold significant proprietary information that AI bots would not be able to replicate. Consultants are also a key point of contact, often liaising between clients and external parties to get a project done, so we struggle to imagine a world where these relationships could be fully replaced. We have gradually added to our positions in these companies in recent times, as their low valuations make us quite comfortable in underwriting the perceived risks today.

We do not try to predict a single outcome, but rather assess where the odds are most favourable, build in a margin of safety, and diversify the strategy across businesses that can create value through a range of environments. This discipline – investing based on probabilities rather than predictions – has guided the results discussed above and remains central to how we have and will allocate capital going forward. In other words, we will not be relying on the Super Bowl Indicator anytime soon.