Written by: Richard Fortin and Brendan Harrington

“You can’t predict, but you can prepare” – Howard Marks

Late last year, we wrote an outlook piece that, in part, outlined potential challenges facing equity investors in 2026. The challenges we listed included lofty S&P 500 valuations and excessive market concentration, with a handful of AI-driven stocks accounting for a third of the index’s market capitalization and a disproportionate share of expected earnings growth and capital spending. We also noted macro risks, including a softening labour market, sticky above-target inflation, trade tensions and tariffs, as well as persistent U.S. fiscal imbalances – all contributing to a risky backdrop for 2026. While we had been concerned with geopolitical risks for some time and had articulated these concerns on many occasions, it was not a central concern of ours going into 2026, despite the ongoing Russia-Ukraine conflict. Nonetheless, less than 3 months into the new year, geopolitical risk considerations are now top of mind for most investors. In fact, the ongoing events in the Middle East offer a timely reminder that risks, even those perceived to be low probability events, are ever-present across market cycles. Nonetheless, predicting geopolitical outcomes is inherently difficult (if not impossible), while making large, concentrated portfolio bets based on these outcomes carries a low probability of success. Preparing for unforeseen events should occur at the portfolio construction phase – not in the middle of a crisis. An all-weather approach means preparing for unexpected market developments by building portfolios comprised of resilient, adaptable businesses that trade at reasonable valuations, while also resisting the urge to make large binary bets on specific outcomes that are inherently difficult to predict and could potentially impair capital in the process.

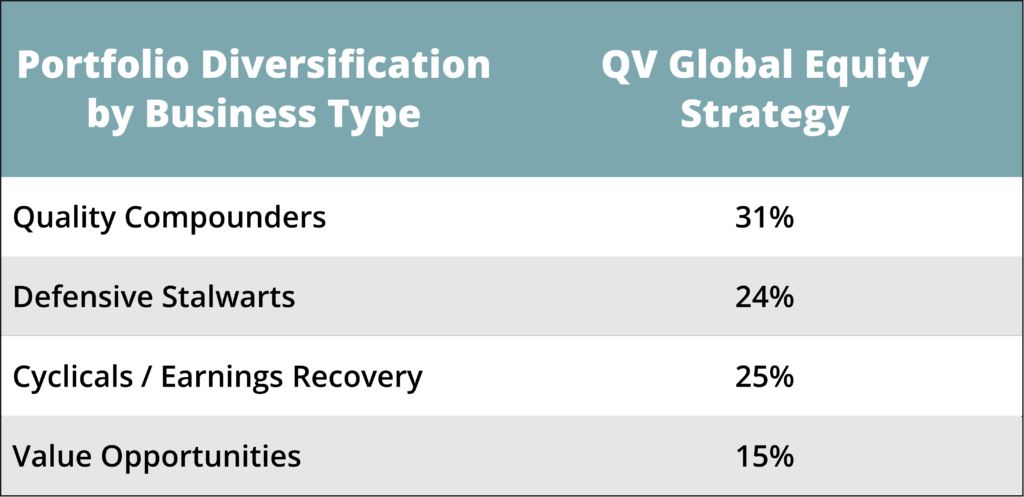

QV’s Global Equity Strategy seeks to diversify risk across individual holdings and market sectors. However, we also seek to diversify holdings across business models and the nature of the opportunities we pursue, including earnings growth potential and valuation discounts. Categorizing portfolio holdings by these criteria provides a better understanding of how our strategies could perform as risks evolve across market cycles. From a business type standpoint, the holdings of our global equity strategy incorporate a mix of Quality Compounders, Defensive Stalwarts, Cyclicals and Value Plays – with each business type playing a specific role within the strategy:

Quality Compounders are among the highest-quality franchises held in our portfolios. They tend to generate above-average returns on capital due to durable competitive advantages and offer above-average growth and long-term compounding potential. However, these businesses often trade at higher valuations, which reflect their attractive long-term characteristics.

Defensive Stalwarts have persistent, durable franchises supported by high, stable profit margins and free cash flow generation. They can provide a strong portfolio ballast and downside protection but only offer average long-term expected growth prospects. This group of businesses seldom produces outsized returns in ‘risk on’ market environments.

Cyclicals offer strong return potential, as their valuations can fluctuate significantly over an economic cycle, but the timing and magnitude of an eventual earnings recovery introduces a source of uncertainty and risk that needs to be accounted for.

Value Plays usually present the most attractive starting valuations and offer a wide margin of safety, but risks can include failed turnarounds or catalysts which fail to materialize, producing significant opportunity costs.

Current portfolio holdings within our global equity strategy fall in the following business type categories (% of capital invested):

Source: QV Investors, as of February 28, 2026

The table illustrates that our global equity strategy is constructed for steady compounding with some downside protection and cyclical optionality. The sizeable allocation to quality compounders is earmarked for value creation – relying on higher quality and durable businesses to generate strong returns over the long-term. However, when combined with the weighting of defensive stalwarts (resulting in an allocation of 55% within compounders and stalwarts), it highlights how our strategy is skewed toward lower-risk, higher-certainty outcomes. We believe this combination of quality and value, diversified across business types, positions the strategy to deliver solid risk-adjusted returns with comparatively lower downside risk over a full market cycle.

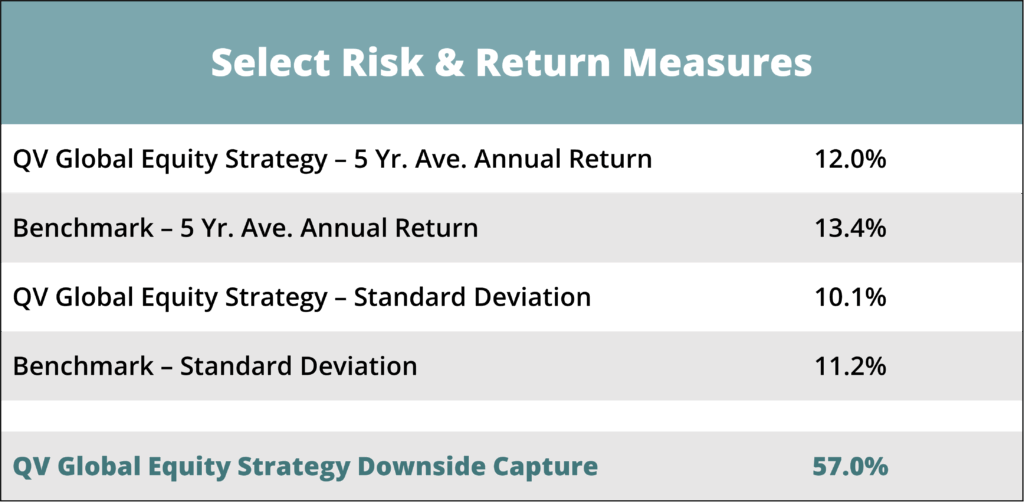

The table below, which outlines select portfolio risk and return measures achieved over the most recent trailing 5-year period, corroborates these desired portfolio attributes:

Source: Morningstar, as of February 28, 2026

Over this trailing 5-year period, our global equity strategy has produced market-competitive returns while taking on much less risk than its benchmark. Moreover, during periods of market volatility, the portfolio captured comparatively lower downside than the broader market.

QV Global Equity Strategy – Recent Initiations

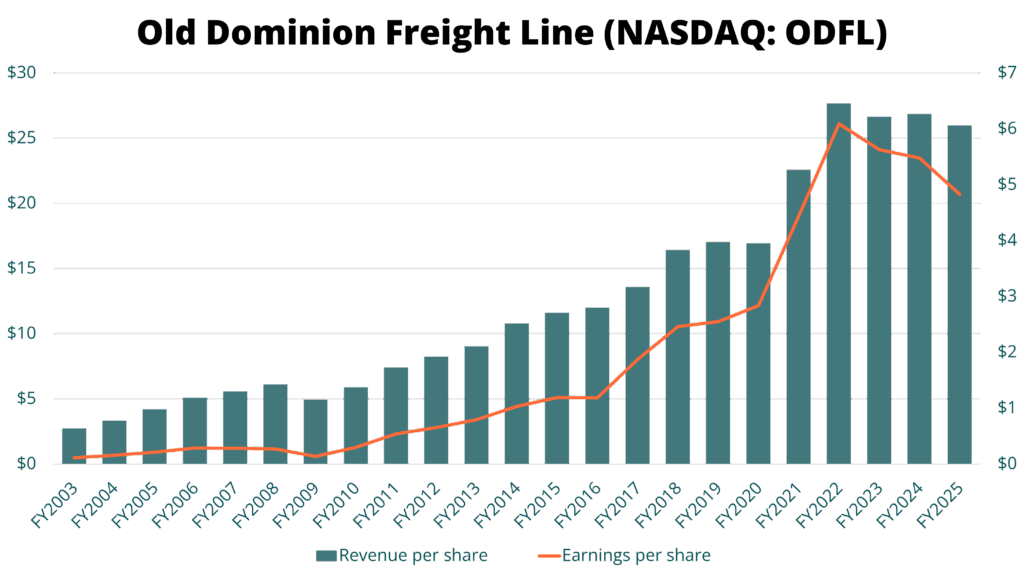

Late in 2025, our global equity strategy initiated a position in Old Dominion Freight Line (NASDAQ: ODFL) at a time when the valuation was at the long-term median on what remain cyclically depressed earnings due to a protracted U.S. freight recession. ODFL is the undisputed best-in-class operator within the U.S. less-than-truckload (LTL) transport industry. ODFL has a durable competitive moat built upon its superior infrastructure density, owner-operator culture and reputation for exemplary service. The company has patiently developed and nurtured these core franchise elements for several decades, resulting in industry-leading profitability, returns on capital and total shareholder returns. ODFL’s business exhibits some cyclicality, but the franchise has been a solid quality compounder over several decades.

Source: Company documents, QV Investors

Despite having to navigate a U.S. freight recession that is entering its fourth year, ODFL remains laser focused on persistently improving its efficiency, customer value proposition and competitive advantage, all whilst maintaining a pristine balance sheet. Whilst we cannot predict the timing of a LTL volume recovery, we can have conviction that a diverse portfolio of best-in-class franchises like ODFL, purchased at reasonable valuations, will provide superior downside protection and above-average full-cycle earnings power.

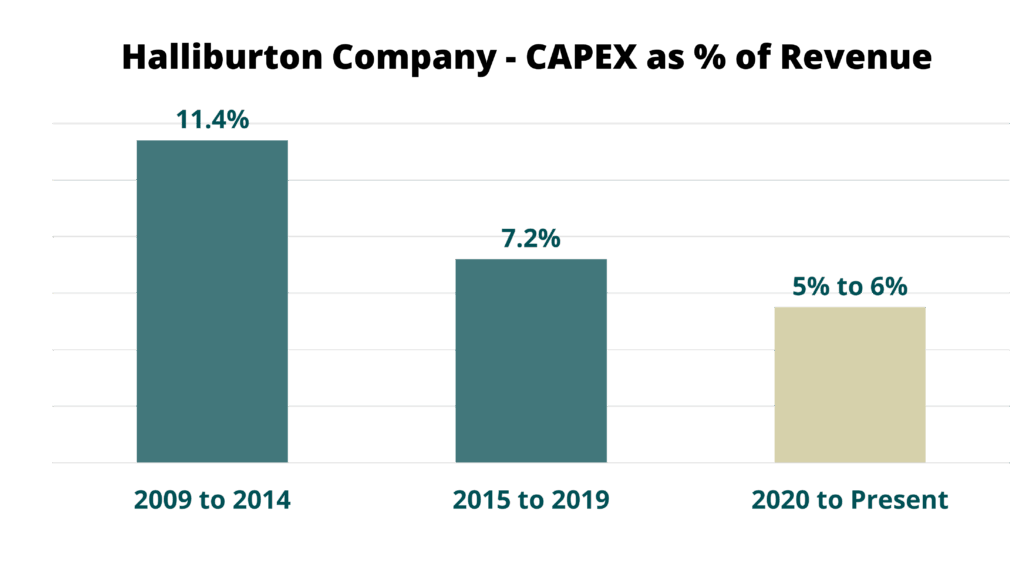

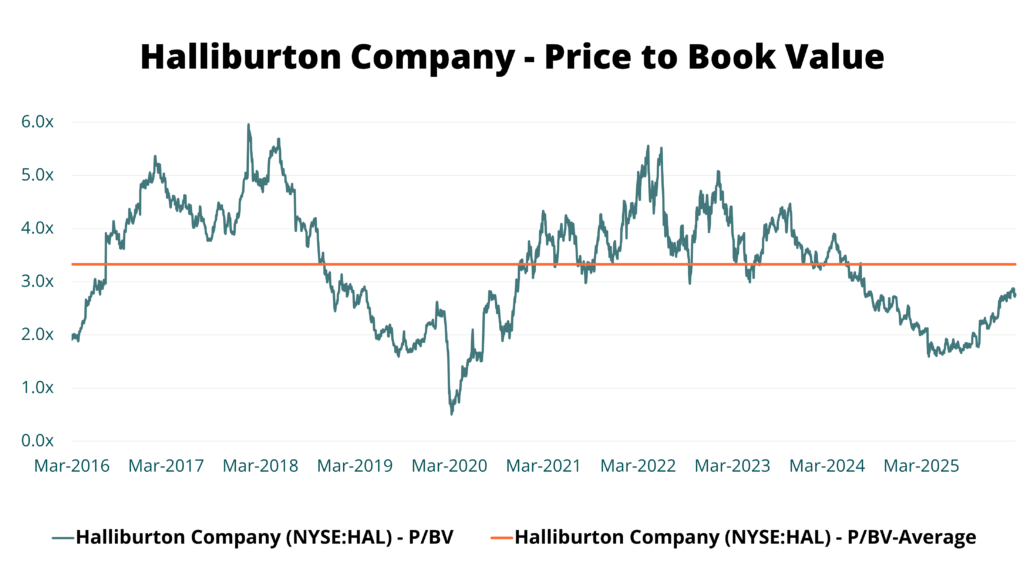

We also initiated on oilfield services (OFS) provider Halliburton Company (NYSE: HAL) in our global equity strategy in the last six months. The company is among a select few diversified OFS franchises offering a full suite of products and services around the globe with a level of scale and technology leadership matched by few competitors. HAL’s customer base includes some of the largest oil and gas producers by market cap and production volume around the world, with a strong presence in North America, Latin America and the Middle East. Since 2019, the company has delivered notable profitability improvements, nearly doubling operating margins in its Completion and Production Services segment and more than doubling them in its Drilling and Evaluations segment. Although global capital spending has increased ~13% over this timeframe (i.e. with positive operating leverage explaining some of the gains), most of the improvements have been driven by a shift in operating strategy – moving away from prioritizing volume and market share to a return-driven philosophy centered on capital discipline and technology-led efficiencies. We expect operating margins to expand again in 2026 and beyond, as HAL continues to execute on its return-driven operating philosophy while also implementing additional cost-saving measures.

On the capital allocation front, management has enhanced its approach through better capital discipline – reducing capex to approximately 5% of revenue (vs. 10%+ a decade ago) and stepping up capital returns to shareholders, with buybacks and dividends now accounting for 50% or more of free cash flow. This refined approach should result in an average annual share count reduction of 4.5% over the next five years.

Source: Company documents, QV Investors

Lastly, HAL shares were acquired slightly above 2x book value – a level near cyclical lows and one that represents an attractive entry point relative to the company’s average valuation multiple and the improving fundamental trajectory of the franchise.

Source: Capital IQ, as of March 2026

In summary, QV’s balanced approach to portfolio construction has always produced a diversified group of high-quality, resilient franchises, built around a reasonable margin of safety to navigate a wide range of risk environments. Although predicting which risks will come to the fore in a market cycle can be a difficult exercise, preparing for unforeseen events through sound portfolio construction is the ultimate ‘all-weather’ approach.