Traditionally associated with the view that the United States is a unique and superior nation for historical and ideological reasons, the phrase “American exceptionalism” has more recently been used to refer to continued outperformance by both the U.S. economy and the U.S. stock market. As other large, developed countries see their GDP growth rates slip towards zero, the U.S. continued to muster growth above 2.5% in 2024. Simultaneously, as we discussed in a previous article, the S&P 500 delivered its second consecutive year of +20% returns in 2024, managing to outperform European stocks by over 20%, the most in over 25 years. Given the apparent strength of the U.S. economy and stock market, you might wonder why the QV Global Small Cap Strategy only holds a ~13% weight in U.S. equities? We dive into this topic below, along with some thoughts on the looming tariffs to be imposed on Mexico, Canada and China by the Trump administration.

Parsing through the U.S. Small Cap Market

The U.S. small cap market (defined for this purpose as stocks with a USD market capitalization between $200 million and $5 billion) is comprised of approximately 1,900 individual stocks.

As a first hurdle for evaluating investments at QV, we like to consider companies with relatively clean balance sheets. As we will discuss later, in the context of an increasingly uncertain macroeconomic environment, minimizing balance sheet risk provides individual companies with the flexibility to withstand and outlast various outcomes. Within the QV Global Small Cap Strategy today, half of our holdings have no net debt. Conversely, only 674 of the ~1,900 aforementioned stocks (36%) have financial leverage of less than 3x net debt-to-EBITDA (earnings before interest, tax, depreciation and amortization). In only very select situations would we consider an opportunity with leverage above 3 times EBITDA (a regulated utility like ONE Gas Inc., with 100% rate-regulated cash flows, is one such exception).

What about returns? As of December 2024, the QV Global Small Cap Strategy maintained a 4-year average return on equity (ROE) of 15%. If we apply a 15% 4-year average ROE hurdle to our already truncated universe of 674 U.S. small cap stocks, 207 companies remain. Stated differently, only 11% of the U.S. small cap market maintains an arguably reasonable leverage position that also enhances the QV Global Small Cap Strategy’s medium-term return on equity.

What about value? The trailing price-to-earnings multiple for the QV Global Small Cap Strategy was 18.6 as of the end of 2024. If we layer this hurdle onto our screening efforts, we are left with 90 stocks. To summarize, there are only 90 U.S. small cap stocks with leverage positions limited to 3 times their EBITDA generation, 4-year average returns on equity greater than 15% and trailing price-to-earnings less than the strategy’s valuation level. Clearly, the breadth of high-quality opportunities in the U.S. small cap market is narrower than you might expect.

What does the QV Global Small Cap Strategy own in the U.S.?

One of our 5 U.S.-domiciled small cap stocks is NV5 Global Inc., an engineering consultant that provides professional solutions for clients across infrastructure, utilities, real estate and geospatial end-markets. Over time, NV5 has delivered impressive growth rates, with earnings per share increasing at a 10-year compounded annual growth rate of 15%. This has partly been driven by mid-single-digit organic growth, further complemented by acquisitions of small engineering businesses in the niches NV5 serves. The company has also expanded into geospatial services, a higher-growth, higher-margin segment of the business, where it sells both geospatial mapping and software analytics to customers looking to better understand certain geographies (think of a utility customer using an aerial snapshot to better understand vegetation growth around its network). The business is led by long-time executive chairman Dickerson Wright, who personally owns 11% of the shares outstanding and has a proven record of thoughtful capital allocation and capital structure decisions in the past. Today, NV5 has a net debt-to-EBITDA position of 1.5x and is currently trading at 14.5x 2025 estimated earnings. The stock has recently been under some pressure, as we assume investors may be spooked by the rhetoric of “shrinking government” coming from the new U.S. administration (i.e. the newly formed “Department of Government Efficiency”). We think this view is too simplistic, and that areas served by NV5, such as consulting on repair work for Departments of Transportation, will need to proceed regardless of political ambitions. Within the QV Global Small Cap Strategy, we believe NV5 Global Inc. provides exposure to the U.S. market without sacrificing tenets of reasonable quality attributes and value.

A Word on Tariffs

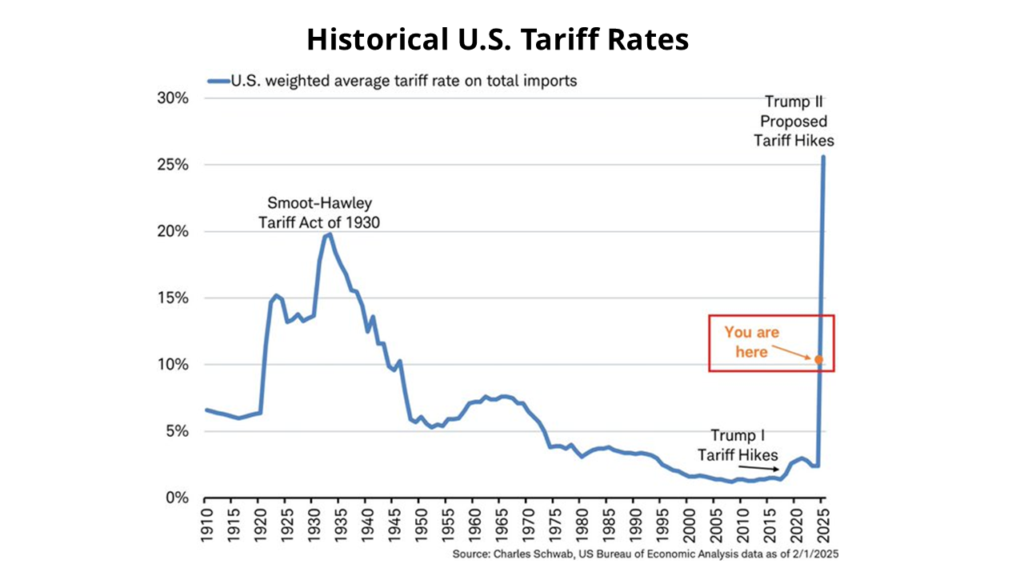

On February 1, news broke from the Trump administration that it would impose tariffs on Mexico, Canada and China, set to begin on February 4, 2025. Canada would be facing a 25% tariff on all imports, except for energy, which would face a 10% tariff. On February 3, Canada and Mexico announced they had reached last-minute agreements with Trump to pause the imposition of tariffs for at least 30 days. This came as Canada announced measures to appease Trump’s demands surrounding border control and organized crime. It is unclear if improvements in border control and preventing the flow of illicit drugs are really the main goals that President Trump is trying to achieve. In any case, it stands to reason that the U.S. is trying to extract more and more from its trading partners. We believe the structural trade relationship between the U.S. and the rest of the world is changing and that once-friendly relationships and alliances may be shifting.

What we do know is that taxes on imported goods create near-term inflationary pressure, disruption for supply chains and lower economic growth. We also know that the U.S. is operating from a position of relative economic strength. If the magnitude of proposed tariffs do eventually come to fruition, the trade shock would far exceed that from Trump’s first term – to a level not observed since the Smoot-Hawley tariffs of the 1930s. However, there is a lot we still don’t know, including duration, timing and policymakers’ responses (in terms of the full scope of possible retaliation from governments, as well as forms of fiscal and monetary policy support).

What is clear is that uncertainty is increasing and that which appeals to reason and logic may not prevail. As the events of recent days highlight, the “facts” can seemingly change on a day-to-day basis. It begs a question that executives of our portfolio holdings must have on their minds; how does one even begin to conduct business against this backdrop? We think it seems likely that large capital projects may be curtailed or that required rates of return will increase to account for the heightened uncertainty.

Long-term ownership of high-quality franchises can yield favourable investment outcomes without necessitating short-term tactical shifts to enhance portfolio defensiveness. With a focus on long-term value creation, our portfolio franchises already exhibit characteristics that contribute to overall portfolio defensiveness. Durable balance sheets provide financial flexibility to thrive under a range of challenging economic scenarios, and strong relative growth and cashflow resiliency, when coupled with undemanding valuations, collectively enhance portfolio ballast in more difficult market conditions. We will, however, always look to be opportunistic when we feel short-term volatility causes market prices to diverge from our estimate of businesses’ underlying earnings power. A continued focus on risk management tools, such as diversification, will be invaluable moving forward.