By late February, resilient equity performance was suggesting Q1 would mark the fourth consecutive quarter of positive returns. Inflation was trending toward target, interest rates were expected to ease further, and corporate earnings were healthy and growing. This tranquil state, however, was disrupted on February 28th as U.S. and Israeli attacks on Iran sent ripples across financial markets, reminding investors that markets rarely move in a straight line.

The effective closure of the Strait of Hormuz, a key narrow waterway that carries about one-fifth of global crude oil supply, led to sharp price spikes in global energy markets, with the price per barrel of Brent crude oil climbing from $72 pre-conflict to $104 by the end of March. This historically rare price shock is not just isolated to crude alone, but to fertilizer, helium and other commodities that are needed globally and are key inputs to critical industries. This raised inflationary concerns and stagflationary risks, particularly for energy importing nations in Asia and Europe. The loss of life throughout this conflict has been tragic. As investors, however, we also recognize that such disruptive events create winners and losers not only across countries but also across businesses and households that may already be struggling with elevated living costs.

Without clear evidence of decelerating growth nor accelerating inflation above target just yet, the Bank of Canada and U.S. Federal Reserve are exercising patience and maintaining policy rates at current levels. Growing inflation and budgetary concerns from the U.S. military campaign weighed on bond yields as they repriced higher in March. As a result, bonds did not provide their traditional safe haven status in this environment, as the FTSE Canadian Universe Bond Index slid -2.0% in March but held in at 0.2% for Q1. Precious metals also declined in the month, with gold and silver slumping -11.6% and -19.9%, respectively. Both metals finished the quarter with net gains however, as the March correction did not fully offset their appreciation leading up to the conflict.

Equity markets were mixed in Q1 2026. The U.S. market, as measured by the S&P 500 TR ($USD), saw a -5.0% decline in March and a -4.3% return in the first quarter. The Canadian S&P/TSX Composite TR Index eked out a positive 3.9% in Q1, buoyed by strong returns from its heavyweight sectors in energy (30%) and materials (10.6%), despite falling -4.3% in March. There were few places to hide for investors as uncertainty ran high. It remains unclear how this conflict will be resolved, even after many reassurances from Washington that attacks are nearing an end.

Historically, most supply-driven oil price shocks have been relatively short lived, with markets recovering in the ensuing months. However, a long-lasting energy shock does have the potential to force an economic setback. With an uncertain timeline towards a lasting resolution, market participants are left questioning whether a larger drawdown is near.

These are unknowns that cannot be answered accurately. The range of outcomes has widened as new risks have increased. Instead of attempting to answer questions that depend on probabilities and extrapolations that may not transpire, a different investment perspective relying on sound fundamentals and a long-term mindset can provide some clarity during periods of uncertainty. Risks and opportunities go hand in hand, and a focus on enduring fundamental factors can help uncover promising investments and increase your odds of an attractive risk-adjusted return.

Staying Grounded in a Long-Term Mindset

The future will always be uncertain. Focusing on what can be controlled through careful security selection and intentional diversification can shift a worried mind to a more prepared mental state. Fundamental research and awareness of current valuations helps develop this mindset.

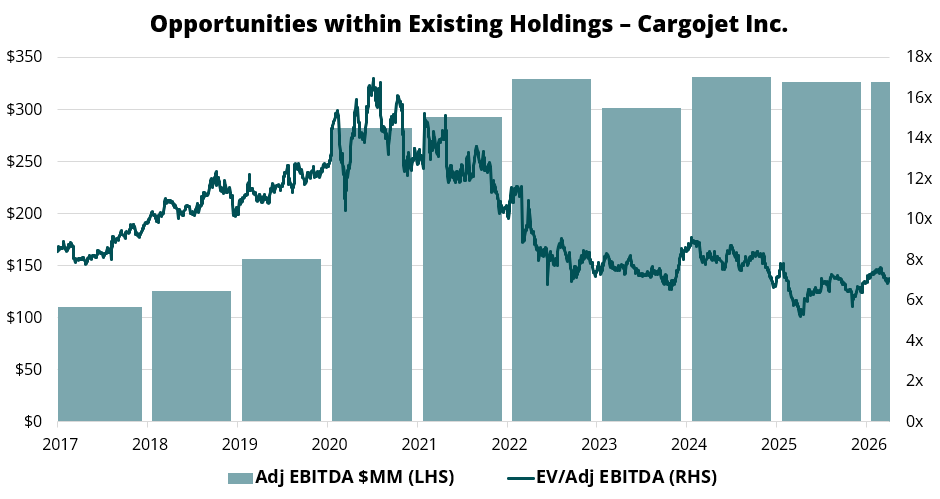

The Canadian small cap team has been recycling capital from some of its takeout successes, such as Guardian Capital, and adding to some of the strategy’s existing positions in materials, health care and industrials. One of these existing positions is Cargojet Inc., with shares that have incrementally cheapened as its international transport services have underperformed expectations recently. Its domestic air cargo franchise remains robust and continues to hold a 90%+ market share in Canada. The majority of its flight services are under contract, providing inflation passthrough protection, earnings stability and growth in shareholder distributions. Its lower valuation provides a margin of safety should cyclical headwinds become a larger factor. At the same time, the current share price offers an attractive valuation for this growing air cargo transport business. Maintaining a long-term focus is not instinctive when market volatility is elevated, but at least it is within our control.

Source: S&P Capital IQ, Company Reports, QV Investors

Opportunities Abound

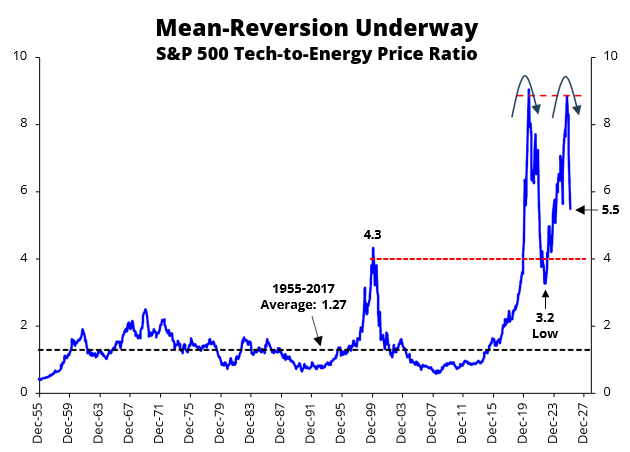

While it can be challenging to pull away from the news headlines about the ongoing war, for long-term investors, notable sector rotations and industry-specific concerns have been revealing interesting opportunities. Technology stocks have been a clear outperformer coming out of the pandemic years. But recently, tech stocks have been under pressure due to several concerns, such as overinvestment in artificial intelligence data center capacity or the displacement of software-as-a-service based businesses by evolving AI capabilities. Conversely, energy stocks have been a clear beneficiary of higher crude oil prices, leading to a sharp sector rotation as shown in the chart below. A re-test of the 2022 low, should the current trend hold, would suggest further pain (tech) and gain (energy) for these two respective sectors.

Source: Scotiabank GBM Portfolio Strategy, Monthly Chart Book, as of April 2026. Calculated (or Derived) based on data from US Indexes ©2015 Center for Research in Security Prices (CRSP), The University of Chicago Booth School of Business, Bloomberg.

Fortunately, our global equity team established a position in oilfield services provider Haliburton in early January. The investment thesis was centered on a low valuation and strong free cash flow generation, despite what was expected then to be sluggish end market demand for its services. Management’s capital allocation discipline was a decisive factor as the team planned for efficiencies to free up additional cash flow for improved shareholder return activity. The shares have benefited from the higher energy price backdrop since then, but the thesis was not reliant on the supply shock. Sometimes the timing just works out for those that are focused from a bottom-up perspective.

The global small cap team purchased a business that was caught up in the AI displacement scare during the quarter. Rightmove PLC is a market share leading digital platform that facilitates 80%+ real estate activity in the United Kingdom. At its core, Rightmove is a data business in the UK real estate market with decades of proprietary data and sufficient scale to innovate and maintain its lead position. AI fears have pressured its shares lower, opening up an attractive entry point as the team believes its data integrity and AI innovations are likely to unlock greater value add, rather than being restrictive to its growth outlook.

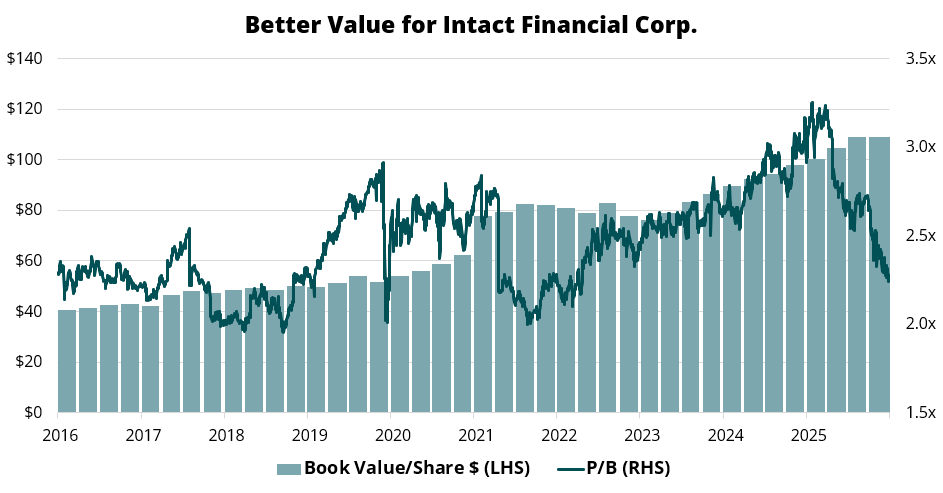

A side beneficiary of the AI boom has been Toromont Industries, an Eastern-based heavy equipment dealer in the Canadian equity strategy. The promise of strong end market demand for its refrigerant cooling business (CIMCO) from overheated AI centers lifted its shares to a level that warranted a trim to manage valuation risk. Proceeds were reinvested in areas that offer better value, such as the shares of Intact Financial. The team has been increasing its position in Intact as concerns of a tougher auto insurance cycle in the U.S. have weighed on its valuation, despite it not having material exposure in U.S. auto insurance. Intact remains a globally diversified and best-in-class P&C insurer. Its current valuation presents another opportunity for mispriced quality.

Source: S&P Capital IQ, QV Investors

Market narratives and investor sentiment have always been in perpetual flux. It is the nature of public markets. Maintaining a fundamental research framework and long-term mindset can help identify opportunities despite prevailing narratives dominating news headlines.

Prepared Flexibility

At the same time, the range of outcomes is wide. White House policy decisions have been unconventional, prone to revisions and will likely have unexpected longer-term consequences. Instead of scrutinizing what is to come, another element within our control is to be prepared for volatility. Preparedness can be a powerful tool to offset emotion during times of market stress, while centering investors back to their long-term investment goals.

Bonds have not yet held in as expected, as the prospect of rising inflation led to higher bond yields (lower bond prices) in March. Credit premiums also saw modest widening, improving the all-in yield for public fixed income. Concerns in the fast-growing private credit market have accelerated in recent months. It is still unclear whether these concerns are overblown, but history has not been kind towards asset classes that have experienced the degree of meteoric issuance that private credit has. Echoes of the U.S. mortgage market leading up to the great financial crisis have intensified as private credit assets have doubled in the past six years alone. It is yet to be seen whether recent investor withdrawals from various private credit funds can be contained within themselves (the base case) or spread across risk markets as contagion mounts. But it does highlight the liquidity demarcation between private and public fixed income, which is an important consideration when assessing their relative value during periods of volatility.

In recent months, the fixed income team has been selectively buying higher-rated corporate and provincial bonds from resilient credits as all-in yields have improved. High quality public fixed income instruments such as these offer vital liquidity to rebalance into cheaper equity valuations, should the current confluence of collective risks lead to a softer economic outlook. Flexibility can also be constructed with shorter maturity treasury bills and well vetted inventory lists, which provide optionality to help navigate periods of wider spread dispersion.

Sustained investment success demands discipline in the ever-present face of market uncertainty. Staying grounded in fundamental research while maintaining a long-term focus are key tenets for patient investors. As well, respecting the need for flexibility and preparing for unexpected events are critical factors that are within control, as the range of outcomes is likely to remain wide for a while longer.